This article first published in GamesBeat, GamesIndustry International and PocketGamer in July 2012.

Digital investment bank Digi-Capital has just published the Q2 Transaction Update of its Global Games Investment Review 2012.

As anticipated when the Review was published earlier in the year, 2012 is proving to be a bumper year for games M&A globally. Although we are only 6 months into 2012, games M&A has already reached 88% of the transaction value of all of 2011 (the previous record year). The first half of the year has also borne out our prediction that the Zynga IPO might be the high water mark for Social Games 1.0 investment. More than ever, now looks like the time for strong independent and larger, more established games companies to consider their strategic options.

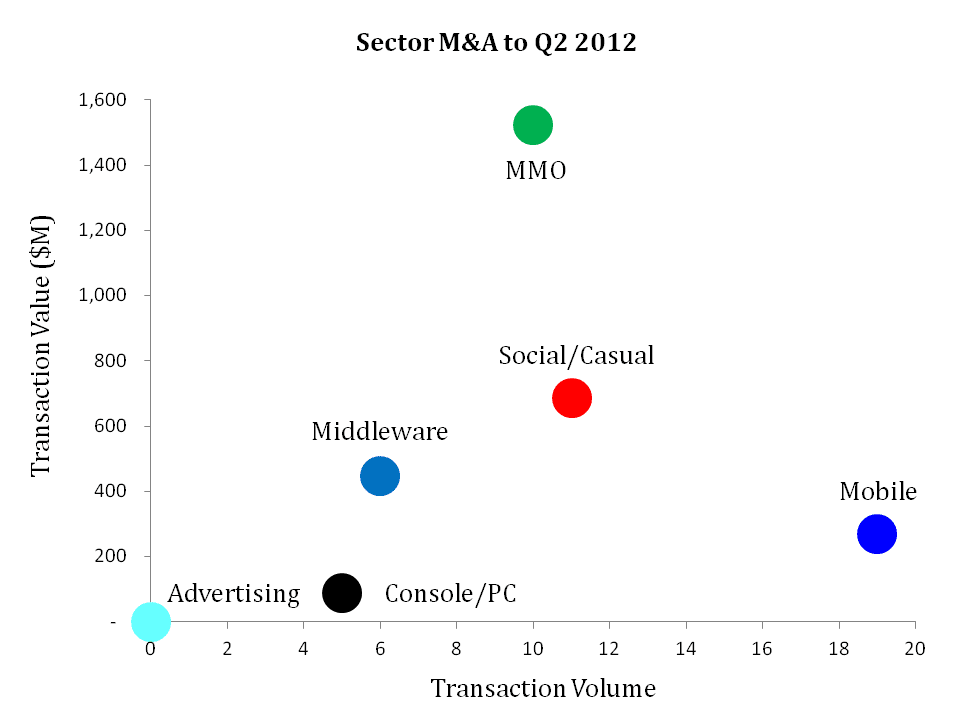

As detailed in the Review, 2011 was a record year for games M&A with 113 transactions generating $3.4B transaction value at an average transaction value of $30M. To Q2 2012, 51 transactions generated $3B transaction value at an average of $59M. The Q2 2012 run-rate for games M&A transactions is 76% higher by value but 10% lower by volume than 2011 because of fewer, larger M&A transactions. As we anticipated at the start of the year, MMO, Social/Casual and Mobile continue to dominate, and we anticipate that this trend might continue through 2012. All global games M&A transactions and public company comparables across sectors are detailed in the full Review.

Again as anticipated, mobile games investment accounted for 31% by transaction value and a significant 49% by transaction volume, and mobile (mobile-social in particular) might continue to be a driving force for games investment through 2012. Games middleware (and gamification in particular) generated 33% of transaction value and 18% of transaction volume. Gamified education and health appear to have become growing investment trends. The success of free-to-play continues to attract investors to MMO, accounting for 22% of transaction value and 12% of transaction volume. Chinese, Japanese and South Korean acquisition and investment continues apace in mobile, mobile-social and free-to-play MMO both domestically and internationally, and we anticipate dealflow to increasingly originate from these markets. All investment transactions and public company comparables across sectors are detailed in the full Review.

Both the dealflow we’re working on and the data we are seeing indicates that independent games companies are actively pursuing the following options by sector:

- Mobile/tablet: fundraising (particularly mobile-social)

- Social/casual: consolidating M&A

- MMO: consolidating M&A (particularly from Asia)

- Console: Strategic Review for online/mobile pivot (generally as a precursor to fundraising or M&A)

- Games Middleware: fundraising or consolidating M&A (particularly gamification and cloud gaming)

- Games Advertising: organic growth

Increasingly we are helping companies with Strategic Reviews prior to advising on fundraising or M&A, as industry growth and transition across sectors present many opportunities and challenges. Similarly we’re helping larger, more established companies from both within the industry and adjacent (particularly gambling companies) as they look for great independents to acquire.

We can’t wait to see what the second half of 2012 might bring!

About Digi-Capital: Digi-Capital is an investment bank focused on high growth digital companies across games, technology, media and telecoms in America, Europe and Asia (China, Japan, South Korea). Digi-Capital’s Managing Director Tim Merel will be presenting on games investment and M&A at both GamesBeat/MobileBeat in San Francisco and ChinaJoy in Shanghai in July.

Disclaimer: This document has been produced by Digi-Capital Limited and is furnished to you solely for your information and may not be reproduced or redistributed, in whole or in part, to any other person. No representation or warranty (expressed or implied) is made as to, and no reliance should be placed on, the fairness, accuracy or completeness of the information contained herein and, accordingly, Digi-Capital Limited does not accept any liability whatsoever arising directly or indirectly from the use of this document. In particular, the inclusion of any financial projections are presented solely for illustrative purposes and do not constitute a forecast. The recipient should independently review the underlying assumptions of the financial projections. This document is intended for initial contact with individuals and entities known to Digi-Capital Limited. This document is intended for use by the individual to whom it is sent, it is confidential and may not be reproduced in any form, further distributed to any other person, passed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose without the prior written consent of Digi-Capital Limited. In the event that you are not the recipient indicated and you have inadvertently received this document, please delete it immediately. This document does not constitute or form part of, and should not be construed as, an offer, solicitation or invitation to purchase, subscribe for, or otherwise acquire any securities nor shall it or any part of it nor the fact of its distribution form the basis of or be relied upon in connection with any contract or commitment whatsoever. Any investment decision should be made solely on final documentation, and then only after review of the diligence materials and consideration of all relevant risks. Digi-Capital Limited does not have any responsibility for the information contained herein and does not make any representations or warranties, express or implied, as to the adequacy, accuracy or completeness of any statements, estimates or other information contained in this document. The information contained herein, while obtained from sources believed to be reliable, is not guaranteed as to its accuracy or completeness. This document may include forward-looking statements, including, but not limited to, statements as to future operating results and potential acquisitions and contracts. Forward-looking statements are sometimes, but not always, identified by their use of a date in the future or such words as “anticipates”, “aims”, “could”, “may”, “should”, “expects”, “believes”, “intends”, “plans” or “targets”. By their nature, forward-looking statements are inherently predictive, speculative and involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. No assurances can be given that the forward-looking statements in this document will be realised. Digi-Capital Limited does not intend to update these forward-looking statements. No securities regulatory authority has approved or expressed an opinion about Digi-Capital Limited’s business prospects or any related securities. Any such securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the "Securities Act"), or any other state or federal securities laws and may not be offered or sold in the United States of America absent registration under the Securities Act or an exemption from the registration requirements thereof. Digi-Capital Limited and any entity referred to in this document have not and will not be registered under the United States Securities Exchange Act of 1934, as amended or the US Investment Company Act of 1940, as amended, and any related securities may not be offered or sold or otherwise transferred within the United States or to, or for the account or benefit of, U.S. persons except under circumstances which will not require Digi-Capital Limited or any associated entity to register in the United States in accordance with the foregoing laws or any other law. Digi-Capital Limited is authorised and regulated by the Financial Services Authority. Digi-Capital Limited is the copyright owner of this document and does not grant you any licence to copy, adapt or distribute it, in whole or in part, without Digi-Capital Limited’s written permission to do so.